Industry Insights: Global Packaging Update Fall 2021

2021 has witnessed remarkable rebounds for the economy generally, the transaction market overall, and specifically for the Packaging Transaction Market. The economy rebounded particularly well through mid-year 2021, with the US GDP growing over 6% in each of Q1 and Q2 and defying the rise of the delta variant, inflationary pressures, supply chain disruptions, and a disconnect between labor demand and willing workers. This success was mirrored in the deal-making marketplace, particularly among financial sponsors (Private Equity), which drove volumes that will surpass 2019's former annual record [i]. Acquirers are riding the high economy, a very favorable lending environment, and sellers seeking to avoid a potential increase in tax rates in 2022.

2021 has witnessed remarkable rebounds for the economy generally, the transaction market overall, and specifically for the Packaging Transaction Market. The economy rebounded particularly well through mid-year 2021, with the US GDP growing over 6% in each of Q1 and Q2 and defying the rise of the delta variant, inflationary pressures, supply chain disruptions, and a disconnect between labor demand and willing workers. This success was mirrored in the deal-making marketplace, particularly among financial sponsors (Private Equity), which drove volumes that will surpass 2019's former annual record [i]. Acquirers are riding the high economy, a very favorable lending environment, and sellers seeking to avoid a potential increase in tax rates in 2022.

Mazzone Advises UMI on its sale to The Dupps Company

Reflecting on the transaction, Jessica Colbert, President and owner of UMI, noted, “We are excited about continuing the legacy of my Dad, Edward Hill, and the next phase of growth for UMI as part of The Dupps Company. We value the long relationship UMI has had with the Mazzone team and appreciate their continued advice and value they drove for us over the years, including through this transaction with The Dupps Company.”

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to Universal Maintenance Inc. (“UMI”) with respect to its sale to The Dupps Company on September 1, 2021.

Reflecting on the transaction, Jessica Colbert, President and owner of UMI, noted, “We are excited about continuing the legacy of my Dad, Edward Hill, and the next phase of growth for UMI as part of The Dupps Company. We value the long relationship UMI has had with the Mazzone team and appreciate their continued advice and value they drove for us over the years, including through this transaction with The Dupps Company.”

Bill Gehr, CFO of The Dupps Company commented, “We are thrilled to help build upon the legacy of UMI and work with Ms. Colbert and the UMI team to continue the strong service and growth of UMI as part of The Dupps Company. Thanks to Mazzone & Associates for its help working with us to facilitate a smooth transaction process from due diligence through closing.”

About Universal Maintenance Inc.

Universal Maintenance Inc. is an engineering, design and construction project management company with an established reputation for providing manufacturing plants a turn-key service solution — everything from engineering, design, fabrication, installation to maintenance. UMI works mostly in the growing poultry industry.

About The Dupps Company

The Dupps Company is a worldwide leader in protein recycling systems and service. From its founding, Dupps has focused on renewable resources, starting with the ‘original recyclers’ — those rendering companies around the world that recycle millions of tons of animal byproducts every year. Dupps offers a comprehensive range of protein co-products processing equipment, service and support for red meat, poultry and fishmeal applications.

Mazzone Advises ValorBridge on its Investment in Brightlink

Sean Dwyer, CEO of Brightlink commented, “We are thrilled to partner with ValorBridge for growth capital as it allows us the flexibility to continue scaling our business and meet growing market demand. This is exciting news for the entire Brightlink team, our customers and our partners. Thanks to ValorBridge’s investment, we will be able to keep up with the growing demand of our market and will have the ability to continue scaling towards a bright future.”

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to ValorBridge Partners (“ValorBridge”) with respect to its investment in Brightlink Communications (“Brightlink” or the “Company”).

Reflecting on the transaction, Christopher Durham, General Manager of ValorBridge, noted, “We are excited about our new partnership with Brightlink and look forward to supporting them in their next phase of growth. The Mazzone team drove value by introducing us to the management team and creatively structuring a win-win deal for us and Brightlink.”

Sean Dwyer, CEO of Brightlink commented, “We are thrilled to partner with ValorBridge for growth capital as it allows us the flexibility to continue scaling our business and meet growing market demand. This is exciting news for the entire Brightlink team, our customers and our partners. Thanks to ValorBridge’s investment, we will be able to keep up with the growing demand of our market and will have the ability to continue scaling towards a bright future.”

Dom Mazzone, Managing Director at Mazzone, noted, “Brightlink has established a solid market position and is poised to benefit from evolving demand for communication tools and services. We are excited to see Brightlink leverage ValorBridge’s capital and resources to continue Brightlink’s exponential growth.”

Founded in 2004 and headquartered in Atlanta, Georgia, ValorBridge is a holding company that owns several affiliated operating companies. ValorBridge’s uncommon combination of substantial entrepreneurial, operational and classic value investing experiences, as well as its long-term orientation as an investment partner, has positioned it as a strong partner in providing capital to growing companies. ValorBridge also offers a wealth of strategic guidance and experience gained from successfully growing companies at all stages of the business life cycle.

Headquartered in Atlanta, Georgia, Brightlink is a leading communications platform and technology company that delivers voice, messaging, analytics, and cloud-based solutions. The Company’s cutting-edge Communications Platform as a Service (CPaaS) platform, cloud-based applications, managed white-label hosted PBX and Unified Communications as a Service (UCaaS) solutions, and network services are used by companies ranging from small to mid-sized businesses to the largest enterprises and communication service providers around the globe.

Market Review: Sustainability in Packaging

In this summary, we highlight trends, developments and M&A activity within the sustainable packaging market including key trends in the supply chain and in regulation, mergers and acquisitions activity, and investment opportunities within the sustainable ecosystem.

Mazzone and Associates understands the key trends and pitfalls in the sustainable packaging market with recent deal experience as well as long-standing industry knowledge. In this summary, we highlight trends, developments and M&A activity within the sustainable packaging market including key trends in the supply chain and in regulation, case studies in mergers and acquisitions activity, and investment opportunities within the sustainable ecosystem.

Recent Packaging Industry Transactions:

Join Our Packaging Mailing List

Enter your email address below to receive our packaging industry newsletters, market reviews, and updates

M&A Insights: Inequity in Sales of Minority, Woman and Veteran Owned Businesses

In order to level set the playing field for minority, woman and veteran owned businesses (“MWVOBs”), those businesses can “check the box” to be given preferential designations to bid for contracts to provide goods or services to the government or large corporations. This has helped MWVOBs drive sales growth they may have otherwise struggled to compete to land.

In order to level set the playing field for minority, woman and veteran owned businesses (“MWVOBs”), those businesses can “check the box” to be given preferential designations to bid for contracts to provide goods or services to the government or large corporations. This has helped MWVOBs drive sales growth they may have otherwise struggled to compete to land.

However, as issue arises when MWVOBs want to sell their business. Often, a significant portion of a MWVOB is derived from them “checking the box.” The dilemma is that most poential buyers of MWVOBs cannot check the same box and, therefore, are legitimately concerned that the revenues derived from “checking the box” will go away after closing. Consequently, most potential buyers either offer lower than market valuations (i.e., lower than market prices) or do not bid at all. A handful of minority and woman owned private equity funds have been formed, but they are capitalists aware of this market phenomenon and try to simply bid slightly higher than already low bids thereby not really providing a better market for these businesses.

My solution is twofold. First, legislatively allow the buyer of a MWVOB to continuing “checking the box” just as the prior owner did, thereby allowing the buyer to pay a more fulsome purchase price at closing to that minority, woman or veteran owner. This solution allows these designations to give more complete value to the owners of MWVOBs and creates more long-term capital for investment by prior MWVOB owners.

Second, any MWVOB owner who sells, mergers, liquidates or otherwise disposed of her or his business, whether by selling a majority of the shares or assets, can no longer use that designation. The purpose of this provision is to minimize shams and persons who are using this system meant to level the playing field as a new playground for inequity.

This solution is not perfect. This solution is a practical approach to solving a market inequity for owners of MWVOBs without creating additional inequities in the system.

Mazzone & Associates Advises Roplast on its Sale to PreZero

Robert Bateman, retired CEO and co-founder of Roplast, reflected on the transaction: “We are quite satisfied with the result and Roplast’s new partnership with PreZero. In these uncertain times, the Mazzone team proved invaluable, providing guidance and driving the marketing process with domestic and international parties. I doubt whether anyone could have advised us better.”

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to Roplast Industries, Inc. (“Roplast” or the “Company”) with respect to its sale to PreZero US (“PreZero”), a subsidiary of the parent company Schwarz Group, headquartered in Neckarsulm, Germany. The terms of the transaction were not disclosed.

PreZero and Roplast come together just as increasing U.S. legislation will be requiring more recycled content in packaging. As noted by PreZero’s press release, this transaction reflects “PreZero’s business goal to vertically integrate and deliver its closed loop solutions to support the circular economy.”

Robert Bateman, retired CEO and co-founder of Roplast, reflected on the transaction: “We are quite satisfied with the result and Roplast’s new partnership with PreZero. In these uncertain times, the Mazzone team proved invaluable, providing guidance and driving the marketing process with domestic and international parties. I doubt whether anyone could have advised us better.”

Robert Berman, co-founder of Roplast, commented “We are excited for Roplast and its future prospects with its new partner. The Mazzone team did a great job at understanding our business and market position in sustainable packaging. They were extremely thorough and did an outstanding job guiding our team and ensuring the transaction ran smoothly for all parties.”

Jonathan White, Managing Director at Mazzone & Associates, noted “We invested significant time to identify the right partner for our client. We found a great fit in Schwarz and PreZero, as they will build and enhance the sustainable product lines that are important to shareholders, management, and customers.”

Stuart Sanford, Vice President at Mazzone & Associates added “This is a great outcome for all parties. It is even more impressive if you consider that the deal was completed with an international buyer during the COVID-19 pandemic, which disrupted sustainability regulations, supply chains, and customers’ forecasts.”

Founded in 1989, Roplast is a leader in providing sustainable flexible packaging in the form of polyethylene film, bags and other flexible packaging. Based in Oroville, CA, the Company is a leader in providing certified recycled content in its packaging for its customers as well as developing closed loop solutions for the circular economy. Roplast manufactures, converts, and prints its products for a variety of markets.

M&A Insights: Supply & Demand on Valuations in the Capital Markets

The merger and acquisition activity in the capital markets is currently extraordinary, and I believe we could set records for activity level and volumes in 2021.

M&A Insights: The SPAC Boom

There are over 550 SPACS seeking acquisition targets, and that number is rapidly growing.

Industry Insights: Global Packaging Update Winter 2021

With 2020 finally behind us, we can see how the global pandemic impacted the packaging industry and, more specifically, packaging mergers & acquisitions. Overall, Packaging fared better than many sectors of the economy. This was in part driven by a large portion of packaging destined for inelastic markets such as food, personal care, and healthcare as well as a favorable raw material environment for the better part of the year. However, a deeper dive into the various packaging end markets leads to a wide array of year-over-year results for sales and volumes.

With 2020 finally behind us, we can see how the global pandemic impacted the packaging industry and, more specifically, packaging mergers & acquisitions. Overall, Packaging fared better than many sectors of the economy. This was in part driven by a large portion of packaging destined for inelastic markets such as food, personal care, and healthcare as well as a favorable raw material environment for the better part of the year. However, a deeper dive into the various packaging end markets leads to a wide array of year-over-year results for sales and volumes.

Mazzone & Associates Advises iVision on its Sale to CIVC Partners

Reflecting on the transaction, David Degitz, Managing Member of iVision, noted, “We are excited about our new partnership with CIVC and their ability to help us achieve our growth goals. The Mazzone team proved to be invaluable in conducting their marketing process through these uncertain times. Their team tailored the process, notwithstanding limitations of travel due to COVID, to ensure we found a high-quality partner that would close with speed and certainty.”

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to iVision, Inc. (“iVision” or the “Company”) with respect to its sale to CIVC Partners (“CIVC”) in partnership with management.

Reflecting on the transaction, David Degitz, Managing Member of iVision, noted, “We are excited about our new partnership with CIVC and their ability to help us achieve our growth goals. The Mazzone team proved to be invaluable in conducting their marketing process through these uncertain times. Their team tailored the process, notwithstanding limitations of travel due to COVID, to ensure we found a high-quality partner that would close with speed and certainty.”

Gabe Damiani, Managing Member of iVision, noted, “We began planning this transaction with the Mazzone team several years in advance. They became well-versed in our business and acted as an extension of our team, which yielded an efficient process despite challenges due to COVID with respect to deal making.”

Andrew Roche, a Vice President with CIVC, commented, “We are thrilled to partner with David, Gabe and the rest of the management team to grow an already clear leader in the IT managed services space. The Mazzone team did a superb job making the transaction efficient for all parties throughout the deal.”

Dom Mazzone, Managing Director at Mazzone, noted, “David and Gabe have built a world class organization at iVision. It was an honor to work with their team and help select a partner that aligns with their culture and values. We believe iVision and CIVC are poised for tremendous success in their new partnership.”

Headquartered in Atlanta, Georgia, iVision is a leading managed services and technology consulting provider for mid-market and enterprise clients. The Company supports clients across the globe and possesses deep expertise in the legal vertical. Over the last 16 years, iVision has established itself as a premier managed services provider, serving the complex cloud, data center, networking, security and application needs of its clients.

CIVC Partners is a Chicago-based private equity firm investing in high growth middle market companies in business services sectors. Since 1989, the team has invested approximately $1.8 billion in 67 platform companies and currently invests from CIVC Partners Fund V.

Industry Insights: Global Packaging Update Summer 2020

As we now enter the seventh month of our pandemic-induced recession, we find ourselves still dominated by uncertainty – uncertainty in our COVID-19 recovery timeline, uncertainty in our economic recovery, and uncertainty about the long-term impacts of changes in how society will operate in the future. With several months of data now available, we can now begin to assess how has this impacted M&A for the Packaging Industry.

As we now enter the seventh month of our pandemic-induced recession, we find ourselves still dominated by uncertainty – uncertainty in our COVID-19 recovery timeline, uncertainty in our economic recovery, and uncertainty about the long-term impacts of changes in how society will operate in the future. With several months of data now available, we can now begin to assess how has this impacted M&A for the Packaging Industry.

ValorBridge Partners' “Extending the Drive" Non-Control Equity Program

Mazzone & Associates is assisting ValorBridge Partners (“ValorBridge”), an investment holding company, in identifying opportunities to provide business owners with a new source of streamlined non-control equity capital in its “Extending the Drive” Program.

Mazzone & Associates is assisting ValorBridge Partners (“ValorBridge”), an investment holding company, in identifying opportunities to provide business owners with a new source of streamlined non-control equity capital in its “Extending the Drive” Program. The objective is to allow companies to sustain operations and capitalize on interesting growth opportunities which may exist despite the recent market disruption. As Vince Lombardi once said, “People who work together will win, whether it be against complex football defenses, or the problems of modern society.”

For over 20 years, ValorBridge has been providing capital to business owners. The “Extending the Drive” Program targets non-control equity investments between $3 million and $15 million. The proceeds can be used to refinance existing indebtedness as well as provide funding for working capital, growth opportunities or capital expenditures to support existing operations.

“Extending the Drive” Key Terms*

First Down: Targeted closing in 25 days

Second Down: Borrower may repurchase after 25 months at fair market value

Third Down: Convertible into up to 25% of the common equity depending on the company’s valuation

Fourth Down: Deployment of needed funds out of a $100 million pool allocated for the Program

*Other terms to include: Structured as minority preferred equity with dividends (six months PIK-only, then 50% cash, 50% PIK) to allow companies time to manage through the pandemic.

We promise a quick response, an efficient diligence process and, most importantly, a committed partner for you or your clients. ValorBridge is investing using private capital funded by its operating companies like ApolloMD, Crown Asset Management and Guardian Fueling Technologies, which ValorBridge has helped grow for decades. Therefore, there are no limited partners (LPs), debt providers nor other outside stakeholders that need to approve the deployment of capital. ValorBridge stands behind what it says and seeks to leave its businesses on stronger footing when it is time to exit.

ValorBridge believes in leaning into growth, even amidst uncertainty like the current pandemic. An investment now from ValorBridge Partners would provide the added benefit of future financing capability for any potential business needs.

Investment Criteria

Headquartered in U.S.

Industries of Interest:

Business Services

Industrial Services

Niche Manufacturing

Value-added Distribution and Logistics

Industries of No Interest:

Restaurants/Hospitality

Real Estate

Consumer Products

Healthcare Services with Reimbursement Risk

Preference for family-owned or entrepreneur-led businesses with barriers to entry

Please contact us if you are or become aware of any situations where ValorBridge’s capital may help.

Doing Our Part to Help: Pro-Bono Counseling

Our team at Mazzone & Associates is currently offering pro bono consulting and advisory support for businesses struggling through the COVID-19 crisis. Whether you are part of a family-owned business or a sponsor with a challenge at a portfolio company, please let us know if we can help you in any way.

Our team at Mazzone & Associates is currently offering pro bono consulting and advisory support for businesses struggling through the COVID-19 crisis. Whether you are part of a family-owned business or a sponsor with a challenge at a portfolio company, please let us know if we can help you in any way. A few ways we can help may be:

Cash flow forecasting and management;

Strategy for managing conversations with lenders, suppliers, customers, etc.;

Evaluating potential debt or equity capital options;

Providing introductions to resources that may be able to help; or

Providing our deep knowledge and experience to discuss ideas.

We're happy to hold quick phone calls or spend more meaningful time -- please let us know what we can do to help. If you, one of your clients, or one of your friends could use a hand, please do not hesitate to reach out to any of us to set up a time to speak.

We hope that you, your family, and your teams are staying healthy. We look forward to getting through this together and getting back to normal as quickly as possible.

Best regards,

Dom Mazzone

2020 Q1 Industry Insights: Packaging

As of this writing, we are in the early stages of “lock down” as a result of the COVID-19 outbreak. While we cannot be certain of either the severity or duration of the impact, it is safe to say that no one in our Industry is immune to COVID-19’s effects.

Upcoming Industry Events

AWA Global Release Liner Conference, February 27-28 (Presentation Available upon Request)

AIMCAL Executive Conference Webinar, April 9

Packaging M&A Webinar, May 18

International Sleeve Label Conference, November 2

PACKAGING M&A OVERVIEW

As of this writing, we are in the early stages of “lock down” as a result of the COVID-19 outbreak. While we cannot be certain of either the severity or duration of the impact, it is safe to say that no one in our Industry is immune to COVID-19’s effects. Anecdotally, within the last two weeks:

A client serving the retail market is adjusting its customer mix as the shift from brick-and-mortar to online shopping accelerates in the near term

An overseas client is deferring strategic acquisition plans until the impacts of the virus become clearer

A packager of household cleaners is enjoying record volumes and is now seeking to acquire capacity

A packaging equipment client is reassessing timing of capital needs following the postponement of an industry conference to 2021

Overall, Packaging should be less impacted than many other sectors of the market, as (i) it is largely a “local business” with relatively less cross-border or cross-region shipping and supply chain reliance, and (ii) large portions serve cycle-resistant markets such as food & beverage, healthcare, and personal care. Given this, we suspect that Packaging – and the transaction market behind that – will rebound quickly as the virus subsides. In the interim, we expect deal flow to slow substantially as uncertainty hinders decision making.

Please note that the following data is largely “pre-COVID-19” – the impact of the virus will largely be exhibited in data beginning in March 2020. Nevertheless, it can be used by Buyers and Sellers to understand underlying transaction dynamics for when the market returns.

Before the onset of COVID-19, Mazzone highlighted three key trends impacting Packaging companies’ performance and transaction prospects in 2020:

A benign raw material pricing environment is providing margin tail winds for many converters. Among plastic resins, most all packaging grades fell meaningfully in 2019, with many grades continuing this trend into Q1-2020. Paperboard and Linerboard inputs, while not witnessing the same level of decrease, generally enjoyed flat to slightly down pricing. A softening demand (COVID-19 impact) and decreased energy/freight prices (OPEC/Russia price war) could prolong this environment. Buyers are intensifying their due diligence to ensure that current margins are sustainable in the event of (a) a rebound in raw material costs, and (b) demands from customers to pass along these cost decreases.

The search for more sustainable packaging options has created uncertainty regarding the future of certain packaging formats, most notably single use plastics. This uncertainty was amplified in 2019 as state lawmakers introduced no less than 95 bills related to the regulation of plastic bags alone. The inconsistency of state and municipal regulation (and the ability to effectively enforce them) has added further confusion to the market. Investors are seeking to understand the full extent of the shift, so that they can identify the winners and losers among various packaging formats.

2019 saw continued high leverage among packaging companies. Among public packaging companies, Net Debt / EBITDA continued to inch up, reaching 3.7x versus its three-year average of 2.8x. Among Leveraged Finance Transactions (LBOs), average leverage exceeded 5.0x among all disclosed US transactions (not packaging-specific). This heightened level of leverage is manageable in an environment with both low interest rates and a growing economy. As the latter is now greatly at risk, highly levered companies may find themselves capital constrained and/or exceeding covenants as we enter Q2 and Q3 of 2020.

DEAL VOLUMES & PRICING

As the graph below illustrates, global transaction volumes among industrial companies entered a decline well before COVID-19. In the previous cycle, the prior deal volume peak (2007) fell by 30% in 2009 but rebounded in 2010, generally following changes in GDP. Our most recent industrial deal volume peak, however, was in 2015. Transaction volumes have since fallen in each year despite an overall growing economy (and before any COVID-19 impact). Packaging resisted from this trend. In fact, deal volumes have grown year over year including a 14% increase in deal volume from 2018 to 2019.

2020’s early volumes indicate that this may no longer be holding. Volumes for the first two months of 2020 are down 30% from 2019 – with this is largely pre-dating any impact from COVID-19. While we suspect that this gap may narrow as more data comes in, we believe that COVID-19 will reinforce this negative trend as we enter March and April. Nevertheless, we believe that Packaging deal volumes will suffer less than overall deal volumes given that Packaging is overall a more recession-resistant segment of industrials.

Pricing (as determined by transaction multiples) increased by a half turn of EBITDA over 2018’s levels, with median multiples of 9.1x EBITDA and 1.5x Revenue for 2019. Factors continuing to support high levels of pricing include accommodative leverage, a high level of interest from both financial and strategic buyers, ongoing consolidation in those segments of packaging which remain relatively fragmented, and the underlying attractiveness of an industry that consistently offers resilient margins and GDP+ growth. The sustained healthy pricing in this Seller’s Market may also have contributed to lower transaction volumes in early 2020, as buyers wait for more conducive deal metrics (a Buyer’s market).

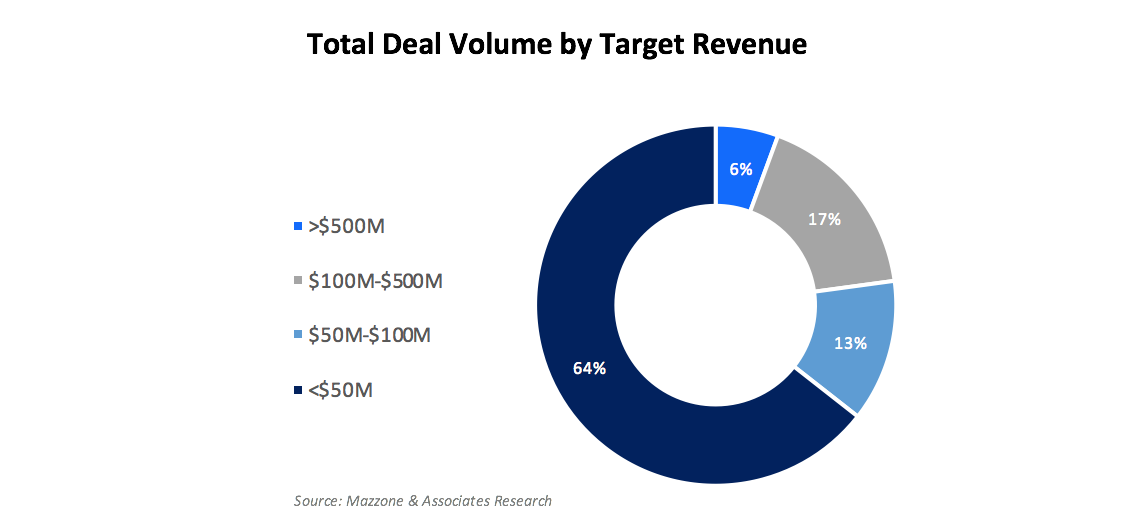

DEAL VOLUME BY TARGET SIZE

There is a healthy market across the spectrum of company sizes, but the greatest activity remains among the smallest companies. Almost two-thirds of disclosed transactions were targets of less than $50 million in revenue, with the majority of these at or below $20 million. While certain sectors such as Glass and Cans have essentially consolidated, there remains tremendous consolidation activity among other sectors, with these smaller tuck-in deals common among paper-based, labels, flexibles, rigid plastics, machinery and distribution companies.

Our analysis indicates that for Pricing, size does matter. Smaller deals (target revenue under $100M) trade at a 1x discount to the overall median of 9.1x. Larger deals, those of targets with revenues above $100 million, trade at a 1x premium (10x+). This differentiation by deal size supports consolidation strategies, as Consolidators seek to arbitrage the multiple expansion to enhance investment returns.

BUYER & SELLER ANALYSIS

Private Equity investors, including both new buyouts and add-ons to existing platforms, accounted for 48% of 2019’s transactions, with Corporate Buyers accounting for 28% and Private Company buyers 24%. These splits are consistent with data from the last five years. We attribute the high participation rate for Private Equity Buyers to:

stable growth and profit margins providing a “defensive investment,”

availability of leverage,

relatively low capex compared to cash generation (particularly in private equity-favored sectors such as Flexibles), and

ability to leverage add-ons and arbitrage size multiples upon exit.

Among Sellers, Private Companies comprised 65% of all transactions, with Corporates and Private Equity splitting the remainder. Private Equity exits are largely to other sponsors, with these secondary transactions accounting for 58% of private equity exits.

As it regards Pricing, 2019 data runs counter to the orthodox view that industry incumbents are better placed to pay higher prices due to their ability to extract synergies from an acquisition. As compared to their corporate and private competitors, financial sponsors pay an additional turn+ of EBITDA, not only for add-ons but also for new platforms. We see this as evidence of their need to deploy capital in a strong seller’s market. The same pricing disparity between Private Equity and other parties exists when the exit their investments, i.e., while Private Equity buyers pay a premium, that same premium exists when they sell (often in secondary buyout to another private equity sponsor).

DEAL MOTIVATIONS

To better understand the drivers for transactions, we identify apparent motivation(s) of the Buyer in Packaging M&A, grouping them into four general categories. The most common motivation is Consolidating Market Share, followed by Product/Market Expansion and Geographic Expansion, and lastly, by Financial (which includes not only Private Equity Platforms, but also IPOs, private investor acquisitions, etc.). Please note that due to multiple potential motivations for a given transaction, the total exceeds the 270 transactions noted for 2019.

The highest valuations include those driven by Financial Motivations (as echoed in our Buyer Analysis for Private Equity acquisitions) and in Product/Market Expansions, which we interpret as the most compelling strategic transactions. Those sectors seeing the most consolidation activity are the Paper, Flexibles, Distribution, and Labels sectors.

SUMMARY

Overall, volume and valuations remained robust in the Packaging M&A space through the end of 2019. Furthermore, several transformative acquisitions have closed/are anticipated to close in 2020:

In Rigid Plastics, Clearlake’s secondary buyout of Pretium Packaging from Genstar Capital

In Flexible Paper, Hood Packaging’s acquisition of TC Transcontinental’s Paper & Woven Polypropylene Packaging operations

In Rigids + Flexibles, Liqui-Box Holdings (Olympus Partners) acquisition of DS Smith’s Plastics Division (as well as the acquisition of certain Rapak operations by TriMas as a regulatory condition of Olympus’ transaction)

In Folding Cartons, Graphic Packaging Holding’s pending acquisition of Greif’s Consumer Packaging Group

In Flexibles, Partner’s Group pending secondary buyout of Schur Flexibles from Lindsay Goldberg

In Rigid Plastics, Silgan’s pending acquisition of Albéa’s Dispensing Business from PAI Partners

In Other Rigids, the pending acquisition of Owens-Illinois Australian and New Zealand operations.

Through 2019 and into early 2020, we continued to see sustained interest in the packaging industry from both strategic and financial investors, as buyers seek to consolidate segments and diversify geographies, markets, and technologies. While the current environment is unsettled, we believe that the underlying trends in in the Packaging space will bring acquirers back to the market as soon as later this year.

NOTEWORTHY TRANSACTIONS

ValorBridge Partners: Efficient Long-Term Capital for the Middle Market

We are hearing that businesses and their owners (from large cap corporates to family founders) are seeking quieter, less-public solutions to achieve their time-sensitive capital needs and objectives.

We are hearing that businesses and their owners (from large cap corporates to family founders) are seeking quieter, less-public solutions to achieve their time-sensitive capital needs and objectives. Mazzone has worked with ValorBridge Partners for almost a decade and is ready, able and willing to help middle market business meet those needs and objectives.

ValorBridge is a long-term investor with over $500 million in assets and significant liquidity across diverse industries. Among its current portfolio of companies are:

ApolloMD, a healthcare service provider focused on hospital emergency rooms;

Crown Asset Management, a financial services business; and

Guardian Fueling Technologies, a provider of turnkey solutions for the fuel distribution industry.

ValorBridge has invested everywhere on the balance sheet from senior debt to mezzanine debt to equity. We focus on the right capital for the business to success and grow, then price the capital to align management with ValorBridge to deliver returns for both as management meets its goals and objectives. All ValorBridge companies are protected with barriers to entry for competitors and have strong management teams.

Please reach out if you are seeking liquidity or structured solutions for debt or equity positions and wish to transact directly and discreetly with an agile, no-nonsense long-term investor. We take great pride in our reputation for speed and certainty despite the current environment, just as we did during the Great Recession.

No one can accurately predict what lies ahead, but we feel the ultimate winners that will emerge from this are the companies and investors that shift the paradigm to prioritize: liquidity, adequate capital bases, and reasonable debt profiles. These three things, along with operational resources that provide some sort of path back to normalcy, will allow us as a nation to successfully emerge through this crisis. ValorBridge and Mazzone intend to lead the way for middle market companies trying to navigate the current storm.

With this unprecedented crisis, much is required of us as a society to address the risks of COVID-19. We must all work together as we traverse through this situation. Please take care and let us all do our part to limit the spread of COVID-19.

Dom Mazzone

Managing Director

Important Update from Mazzone on COVID-19

No one can accurately predict what lies ahead, but we feel the ultimate winners that will emerge from this are the companies and investors that shift the paradigm to prioritize: liquidity, adequate capital bases, and reasonable debt profiles.

No one can accurately predict what lies ahead, but we feel the ultimate winners that will emerge from this are the companies and investors that shift the paradigm to prioritize: liquidity, adequate capital bases, and reasonable debt profiles. These three things, along with operational resources that provide some sort of path back to normalcy, will allow us as a nation to successfully emerge through this crisis.

We are hearing that businesses and their owners (from large cap corporates to family founders) are seeking quieter, less-public solutions to achieve their time-sensitive capital needs and objectives. Mazzone is ready, able and willing to help middle market business meet those needs and objectives.

Please reach out if you are close to stakeholders (large or small) that are seeking liquidity or structured solutions for their debt or equity positions and wish to transact directly and discreetly with an agile, no-nonsense counterparty. We represent several family offices and work with several institutional investors with significant dry powder to invest in private credit and/or equity investments. We take great pride in our reputation for speed and certainty despite the current environment, just as we did during the Great Recession.

Mazzone & Associates is focusing on the health and well-being of our employees. Our firm continues to operate daily and seeks to be vigilant in the education and safety of our team while ensuring the continuity of business operations. This includes working remotely for all employees, as well as stressing the importance of social distancing outside of the firm to slow the spread of COVID-19. The Mazzone team is working very diligently through this crisis and is focused on the implications for all our stakeholders, while trying to help those most in need.

With this unprecedented crisis, much is required of us as a society to address the risks of COVID-19. Our employees are our biggest investment, and their safety, health, and wellness is our top priority. We must all work together as we traverse through this situation. Please take care and let us all do our part to limit the spread of COVID-19.

Dom Mazzone

Managing Director

Mazzone & Associates Advises R. Lee & Associates and Blue Point Capital Partners on the Acquisition of Country Pure Foods

Raymond (“Ray”) Lee, Managing Member of R. Lee & Associates, formerly served in a number of leadership roles at Country Pure, including CEO. He will return to serve as CEO of the Company post-closing, bringing a wealth of executive and industry experience. Reflecting on the transaction, Ray Lee noted, “I’m eager to build on the Company’s outstanding reputation while developing new opportunities to increase product consumption. Mazzone & Associates provided excellent guidance and advice as we navigated the complexities of the transaction process.”

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to R. Lee & Associates and Blue Point Capital Partners (“Blue Point”) with respect to the acquisition of Country Pure Foods, Inc. (“Country Pure” or the “Company”).

Raymond (“Ray”) Lee, Managing Member of R. Lee & Associates, formerly served in a number of leadership roles at Country Pure, including CEO. He will return to serve as CEO of the Company post-closing, bringing a wealth of executive and industry experience. Reflecting on the transaction, Ray Lee noted, “I’m eager to build on the Company’s outstanding reputation while developing new opportunities to increase product consumption. Mazzone & Associates provided excellent guidance and advice as we navigated the complexities of the transaction process.”

John LeMay, a Partner with Blue Point commented, “We are thrilled to partner with Ray and the management team to grow an already clear leader in the better-for-you beverage space. Mazzone proved to be an invaluable advisor throughout the deal.”

Maury Bell, Managing Director at Mazzone & Associates, noted, “Country Pure is a market leader in its category and Ray Lee is a world class operator. We were honored to assist him and the Blue Point team with the transaction.”

Country Pure Foods, Inc. is a leading provider of branded and private label beverage products to healthcare and education markets as well to leading grocery retailers. For over seventy years, Country Pure has been a value-added producer, processer, packager, and distributor of both branded and private label beverages and juice products to the food service, retail, and co-pack end markets. The Company sells its products directly to retailers and through institutional food service distributors into the healthcare and education markets. Based in Akron, OH and with five plants across the U.S., Country Pure has a large geographic footprint to service its diverse portfolio of customers.

Blue Point Capital Partners is a private equity firm managing over $1.5 billion in committed capital. With offices in Cleveland, Charlotte, Seattle and Shanghai, Blue Point's geographical footprint allows it to establish relationships with local and regional entrepreneurs and advisors, while providing the resources of a global organization. The Blue Point partner group has a 21-year track record of partnering with companies in the lower middle-market to facilitate growth and transformative change. It is one of only a few middle market private equity firms with a presence in both the United States and Asia, which provides a distinct advantage for its portfolio companies. Blue Point typically invests in businesses that generate between $20 million and $300 million in revenue.

Mazzone & Associates Advises H&W Printing, Inc. on its sale to Crown Capital Investments

“H&W is a great company and our families are thrilled with the acquisition,” said Christopher Graham, CEO of CCI. “We focus on investing in well-established, market-leading companies and helping them optimize operations, innovate, and grow. The brand, the plant, technology capabilities, and the management team all demonstrate the high-performance attributes we seek within our portfolio companies.”

Crown Capital Investments (“CCI”), a private family office investment firm, has announced its acquisition of H&W Printing, Inc. (“H&W” or the “Company”), a Marietta, Georgia-based provider of full-service marketing solutions.

Mazzone & Associates, as the exclusive financial advisor to H&W, conducted a tailored marketing process to identify prospective buyers that were uniquely suited to partner with management in generating additional growth and success as the Company transitions into new ownership.

Sarah Gossett, President of H&W, opined, “H&W is infused with an entrepreneurial spirit that has propelled us from our humble 1996 print shop beginning to today’s corporate brand projector and marketing production powerhouse operating 24/7.” Ms. Gossett expressed her satisfaction with the transaction when she reflected, “We’re excited to be associated with Crown Capital. They were a natural choice for a management partner to enhance our growth and optimize performance in the corporate marketing support space. Mazzone & Associates worked efficiently and expeditiously to lead the transaction to a close by year-end.”

“H&W is a great company and our families are thrilled with the acquisition,” said Christopher Graham, CEO of CCI. “We focus on investing in well-established, market-leading companies and helping them optimize operations, innovate, and grow. The brand, the plant, technology capabilities, and the management team all demonstrate the high-performance attributes we seek within our portfolio companies.”

Jonathan White, Managing Director at Mazzone & Associates, highlighted, "For over 20 years, H&W has been a flagship example of business innovation and adaptability. We fully anticipate that the tenacity, savvy, and industry expertise of Ms. Gossett's management team, coupled with CCI's established history of successfully vitalizing and streamlining business operations, will facilitate H&W's emergence as a national powerhouse in the corporate brand marketing space."

H&W Printing is a Marietta, Georgia-based provider of innovative, full-service marketing solutions. Since its founding in 1996, the Company has fully integrated its service portfolio to become a true one-stop provider of digital and physical marketing solutions, serving an array of Fortune 500 customers across a variety of end markets.