Key Takeaways from ACG’s M&A South 2025

Mazzone’s senior professionals recently attended the ACG M&A South Conference—a great opportunity across 100+ meetings to stay ahead on current market dynamics shaping private equity and private credit activity. Here we share a summary of our insights:

Mazzone’s senior professionals recently attended the ACG M&A South Conference—a great opportunity across 100+ meetings to stay ahead on current market dynamics shaping private equity and private credit activity. Below we share a summary of our insights:

Increased Appetite in Key Sectors: Across many of our meetings, we observed common investment thesis from the private equity community. There’s growing interest in industries such as automation, advanced materials, environmental services, testing/inspection, and contractual maintenance models. These sectors are becoming increasingly attractive for investors due to their resilience, innovation, and long-term growth potential.

Debt Market Recovery: The debt market is showing incremental improvements, with a notable rise in private credit capital overhang. In 2024, we also saw renewed competition from banks, which positively impacted pricing and terms; however, in the face of tariff concerns and other market uncertainty, we are noticing heightened scrutiny throughout underwriting processes in the early stages of 2025. Additionally, deferred draw term loans are making a comeback as companies seek greater flexibility in an uncertain macroeconomic environment.

Enhanced Diligence Areas: As M&A advisors, we are guiding our clients in highlighting key factors that strengthen their position during diligence. These include:

Substantiating improving margin profiles to showcase operational efficiency.

Ensuring protective measures related to tariffs are well-documented.

Providing clear visibility of growth drivers and projections to instill confidence in potential investors.

As the market continues to evolve, we remain committed to advising clients to position themselves strategically in evaluating options and maximizing long-term value creation.

Investing in the U.S. Fastener Industry: How End Market Resilience and Favorable Attributes Make a Compelling Investment Case

The U.S. fastener industry is a diverse ecosystem of manufacturers and distributors producing and supplying products found in nearly every end market. The products are as diverse as the end markets and applications they serve as fasteners are fundamental to the assembly and integrity of countless products and structures.

The U.S. fastener industry is a diverse ecosystem of manufacturers and distributors producing and supplying products found in nearly every end market. The products are as diverse as the end markets and applications they serve as fasteners are fundamental to the assembly and integrity of countless products and structures.

Areas of focus in our report include:

Macroeconomic Perspective: The U.S. fastener industry operates within a diverse economic landscape shaped by steady end-market demand, public infrastructure initiatives, and shifts in global supply chains.

Industry Outlook: Industry-specific data highlights a mixed but ultimately favorable environment for fastener businesses.

Investment Considerations: Private equity firms and strategic buyers are increasingly drawn to the fastener space due to its fragmentation, ubiquity across end markets, and relatively stable margins.

M&A Trends: Despite broader M&A headwinds since 2022, fastener-related deal activity has remained relatively strong, propelled by consolidators looking to broaden product offerings, expand geographically, and diversify revenue streams.

Operating Initiatives: Whether preparing for an exit or simply focusing on enhancing competitive position, companies across the fastener value chain are pursuing initiatives to improve financial performance, deepen customer relationships, and differentiate themselves.

Mazzone advises MGroup on its recapitalization with Source Capital

Mazzone & Associates (“Mazzone”), a leading investment bank and M&A advisory firm, is pleased to announce that it acted as exclusive financial advisor to the executive team of MFLGH, Inc. (“MGroup” or the “Company”) with respect to the Company’s recapitalization with Source Capital (“Source”). The transaction ensured that the company’s strategic direction remains in the hands of its experienced leadership while providing liquidity to the founders.

Founded in the early-2000’s and headquartered in LaGrange, GA., MGroup™ is a leading brand and provider of building products and solutions in the hospitality, multi-family, student housing and other multi-unit end markets. The Company maintains a broad, unique portfolio of building products and materials for both renovation and new build projects, including shower pans, shower doors, shower surrounds & accessories, custom cabinetry, Ultracera® countertops, sinks, and flooring.

December 2024 Mazzone & Associates (“Mazzone”), a leading investment bank and M&A advisory firm, is pleased to announce that it acted as exclusive financial advisor to the executive team of MFLGH, Inc. (“MGroup” or the “Company”) with respect to the Company’s recapitalization with Source Capital (“Source”). The transaction ensured that the company’s strategic direction remains in the hands of its experienced leadership while providing liquidity to the founders.

Founded in the early-2000’s and headquartered in LaGrange, GA., MGroup™ is a leading brand and provider of building products and solutions in the hospitality, multi-family, student housing and other multi-unit end markets. The Company maintains a broad, unique portfolio of building products and materials for both renovation and new build projects, including shower pans, shower doors, shower surrounds & accessories, custom cabinetry, Ultracera® countertops, sinks, and flooring.

Bo Burdette, CEO of MGroup™, highlighted: “This deal was a significant milestone for our company. Stuart and the Mazzone team played a pivotal role in shepherding the deal through every stage, including structuring the transaction, securing a capital partner, negotiating terms, expediting diligence and facilitating a successful closing. Their understanding of our products and end markets, coupled with their hands-on approach, made all the difference. Our new structure allows us to build on the strong foundation laid by our founders and continue delivering exceptional value to our customers and employees.”

Dave and Patti Murray, who have played pivotal roles in shaping MGroup™’s foundation and growth, expressed their confidence in the new ownership team. “We are incredibly proud of what we have built with MGroup™ and are thrilled to see the company’s future in the capable hands of Bo, Drew, and Scott.”

“We are extremely proud to have played an integral role in this transaction, which underscores our industry and expertise in executing complex transactions,” noted Stuart Sanford, Director at Mazzone. “This deal not only reflects the strong market position of MGroup™ but also highlights the commitment of the executive team to its future. Our team is thrilled to have supported such a dynamic transition.”

Joe Rodgers, Managing Director at Source Capital highlighted “we loved working with Stuart Sanford at Mazzone and Bo to get this over the finish line and are excited to partner with Bo and the other executive team members. MGroup™ has an impressive track record of providing best-in-class products and services to its growing customer base, and we look forward to supporting MGroup™ in this next chapter.”

Williams Business Law served as legal advisor on the transaction.

Founded in the early-2000’s and headquartered in LaGrange, GA., MGroup™ is a leading brand and provider of building products and solutions in the hospitality, multi-family, student housing, and other multi-unit end markets. The Company maintains a broad, unique portfolio of building products and materials for both renovation and new build projects, including shower pans, shower doors, shower surrounds & accessories, custom cabinetry, Ultracera® countertops, sinks, and flooring. Known for its commitment to quality, innovation, sustainability and customer satisfaction, MGroup™ continues to set benchmarks in the Hospitality and Multi-Unit end markets. For more information about MGroup™ and its offerings, please visit www.mgroupcorp.com

Source Capital is an Atlanta, GA based private investment firm that has been providing flexible equity and debt capital to lower middle market companies for over 20 years. The firm has a value-added investing approach that brings (i) patient capital focused on long-term value creation; (ii) collaborative partnerships with management teams, founders/owners, private equity investors and independent sponsors; and (iii) strategic and operational resources to its portfolio companies. To learn more about Source Capital or to discuss a new equity or debt investment opportunity, please reach out to a member of our investment team or visit www.source-cap.com.

Connect with one of our advisors

Enter your email below to connect with a member of our team.

Industry Insights: Global Packaging Industry, Fall, 2024

Through September, 2024 has delivered on the hoped-for rebound in volumes of packaging transactions and stabilization of valuations. While certainly not approaching the peak of activity and pricing seen in 2021, the market has overall been healthier than in 2023.

Through September, 2024 has delivered on the hoped-for rebound in volumes of packaging transactions and stabilization of valuations. While certainly not approaching the peak of activity and pricing seen in 2021, the market has overall been healthier than in 2023.

Our key observations for this edition of Industry Insights:

Through Q3-2024, transaction volumes rebounded by 14% over the same period of 2023, roughly in line with 2022 (-2% vs 3Qs 2022). This improvement occurred in Q1 and Q2, which produced the highest quarterly volumes since 2022.

Third quarter volumes, however, softened slightly. Anticipation of interest rate reductions in both North America and Europe likely held some financial sponsors at bay, and the pending election in the US may also be creating uncertainty which is keeping buyers in the wings. We view these as transitory issues and anticipate additional volume growth in 2025.

Segment outperformers (in volume) were the same as noted in our Winter 2024 edition - Machinery & Equipment and Rigid (non-plastic) packaging. Rigid Plastic Packaging also notched an increase in activity. Those segments with lesser activity include Flexibles and Labels.

On a run-rate basis through Q3, corporate buyers, new sponsor platforms, and sponsor add-ons were less active in 2024 versus 2023. The big change was the appetite from private buyers, which is on pace to double activity in disclosed transactions.

On the limited year-to-date sample, it appears that average deal pricing (as measured by EBITDA multiples) stabilized in 2024 after falling for 2 consecutive years, with multiples roughly equal to 2023’s level.

Over the last five years, premium valuations were observed among Flexibles, Machinery & Equipment, and Rigid Packaging (non-plastic); discounted (less than average) pricing was noted among Distribution / Contract Packaging, Paper, and Labels. This has generally held true in 2024 but with some interesting longer-term trends emerging among the segments.

As noted previously, there remain a number of transactions that have been put “on hold.” The economic and political environments are creating uncertainty which continues to weigh on pricing, and if sellers are looking for a return to 9x+ multiples, it appears that they will continue to wait well into 2025+.

Recent Packaging Industry Transactions

Mazzone advises ValorBridge Partners on its investment in Atlas Carts

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to ValorBridge Partners (“ValorBridge”) with respect to its investment into Atlas Carts (“Atlas”).

Formed in 2022 by industry veterans, Atlas is a fast-growing manufacturer of golf carts and low-speed vehicles. The Company offers a range of all-electric models that are fully customizable for use on and off the golf course.

July 2024 Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to ValorBridge Partners (“ValorBridge”) with respect to its investment in Atlas Carts (“Atlas”).

Formed in 2022 by industry veterans, Atlas is a fast-growing manufacturer of golf carts and low-speed vehicles. The Company offers a range of all-electric models that are fully customizable for use on and off the golf course.

Sanjay Kopay, co-CEO of Atlas commented, “ValorBridge shares our vision of driving growth and becoming a market leader, and we look forward to collaborating with their team.” Mark Messick, Co-CEO of Atlas noted, “We are delighted to partner with ValorBridge as they support us in in the execution of our growth initiatives.”

“We’re excited to partner with the Atlas team. Atlas has already cemented itself as an innovator in the golf cart industry, and we are excited for their future,” remarked Chris Durham, General Manager at ValorBridge.

Dustin Ramsey, Director at Mazzone, noted, “Mark and Sanjay have accomplished in a few years what many spend their entire careers pursuing. We eagerly anticipate the success that their partnership with ValorBridge will bring in this next chapter.”

ValorBridge Partners is an Atlanta-based private evergreen holding company that owns, operates, and invests in companies in a wide range of industries. With a track record spanning over two decades, ValorBridge possesses substantial entrepreneurial, operational, and classic value investing expertise. Its long-term investment orientation has positioned the company as a strong partner in providing capital to growing businesses. ValorBridge also offers a wealth of strategic guidance and experience gained from successfully growing companies at all stages of the business life cycle.

Connect with one of our advisors

Enter your email below to connect with a member of our industrials team.

Director Stuart Sanford Hosts Panel at AWA Virtual Forum

Stuart Sanford, Director at Mazzone, hosted a panel discussion at AWA’s M&A Executive Forum and was joined by executives leading packaging and label companies through M&A and global expansion initiatives. Continue reading to view the recording.

Stuart Sanford, Director at Mazzone, hosted a panel discussion at AWA’s M&A Executive Forum and was joined by executives leading packaging and label companies through M&A and global expansion initiatives. Bringing perspectives of Corporate Investors, CEOs and a leading Investment Banker in Mexico, this panel explored impacts from elevated interest rates, geopolitical risks, near-shoring, ever-changing focuses on due diligence and other topics including:

Major themes impacting M&A in the packaging and label markets

Underlying data on cross-border activity and examples of corporations executing cross-continent strategies.

How the disconnect in public markets and M&A are impacting corporate development decision-making

Impacts from recent trends on due diligence processes

Lessons from expansions into new geographic markets

Impacts from recent elections in Mexico for near shoring trends

How EPR and other sustainability drivers are impacting M&A and investments

Alternatives to traditional M&A for geographic expansion

Equity and debt capital markets support for cross-border M&A and investment in Mexico and Latin America

If you were unable to attend and are interested in learning more about cross-border M&A and dynamics impacting corporate dynamic initiatives in this industry, you may view a recording of the panel below.

Panelists:

Danny Allouche: SVP & Chief Strategy & Corporate Development Officer at Avery Dennison

Virag Patel: CEO of ePac, LLC

Max Baumann: Finance Business Partner- M&A and Manufacturing at ProAmpac

Gilberto Sotelo: Managing Director at Alea Capital

Navigating Cross-Border M&A: A Guide for Key Stakeholders Evaluating Opportunities in North America

This executive summary, crafted from the perspective of an experienced investment banking team, is designed to assist buyers navigating the dynamic landscape of cross-border M&A transactions. In 2022 and 2023, approximately 30% of Mazzone’s transactions were cross-border, with Mazzone advising clients from the U.S., Europe, the Middle East, and Asia, in the closing of transactions in the U.S., Mexico, and Europe. From understanding the dynamics and common pitfalls to implementing strategies for success, this guide aims to empower business leaders to make informed decisions and navigate the complexities where a buyer based in Europe, the Middle East, Asia, South America or Africa is looking to acquire a North America-based business.

Executive Summary

This executive summary, crafted from the perspective of an experienced investment banking team, is designed to assist buyers navigating the dynamic landscape of cross-border M&A transactions. In 2022 and 2023, approximately 30% of Mazzone’s transactions were cross-border, with Mazzone advising clients from the U.S., Europe, the Middle East, and Asia, in the closing of transactions in the U.S., Mexico, and Europe. From understanding the dynamics and common pitfalls to implementing strategies for success, this guide aims to empower business leaders to make informed decisions and navigate the complexities where a buyer based in Europe, the Middle East, Asia, South America or Africa is looking to acquire a North America-based business.

Common Motivations for Cross-Border M&A in North America

In an era marked by globalization, overseas business owners are increasingly exploring opportunities to expand their portfolios by acquiring businesses in North America. The North American market, renowned for its innovation, diverse industries, and robust economy, offers an enticing landscape for strategic acquisitions. Below are a few common motivations we have observed in recently closed transactions where international leadership teams are looking to enter or expand their footprint into North America.

Near-shoring Trends in a Post-COVID world: Mentions of reshoring in earnings calls were up 128% in the first quarter of 2023, compared with first quarter of 2022. From 2019 to 2023, there was a 23% decline in U.S. companies that list China as a top 3 sourcing country. In 2023, Mexico surpassed China as the largest exporter of goods to the United States.

Customer Supply Chain Demands: “Made in the U.S.” and proximity to North America customers are key motivations whether the Buyer sees this as an opportunity to de-risk supply chain, capture additional wallet share or potentially just maintain business with its current customer base.

Economic Diversification and Global Expansion: Overseas companies, seeking to diversify their revenue streams and expand their global footprint, were increasingly looking towards North America, which represents one of the world's largest and most dynamic markets.

Enter your email address below to continue reading

Spotlight: Cross-Border Transactions in the Packaging Industry

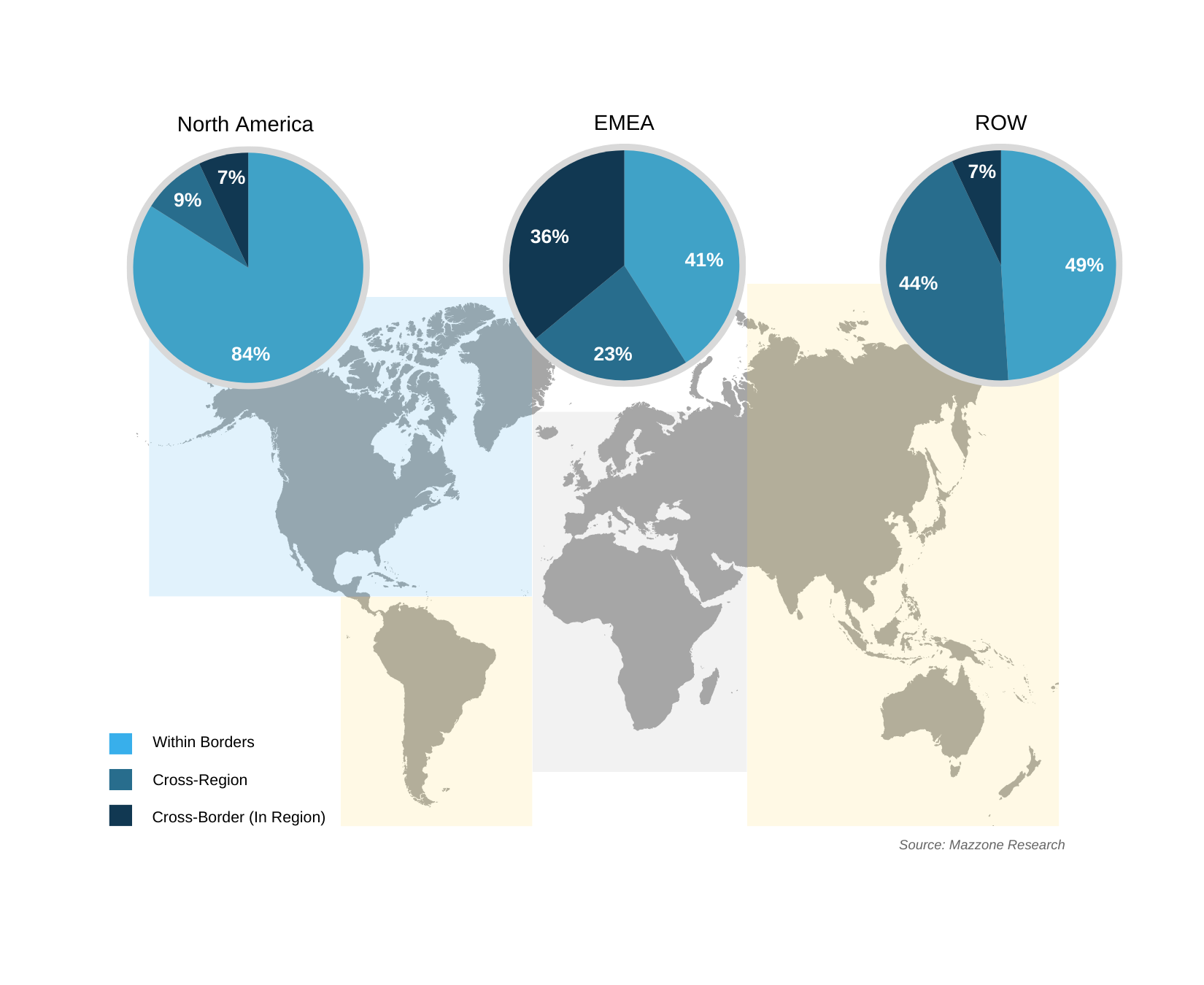

Mazzone’s Packaging Deal Database tracked 70 cross-regional transactions in 2023, which is on par with 2021 and 2022 at 18% of the overall sample. Including cross-border transactions within regions shows a much more active cross-border marketplace, totaling 142 transactions (40% of all Packaging Transactions in 2023).

Mazzone’s Packaging Deal Database tracked 70 cross-regional[1] transactions in 2023, which is on par with 2021 and 2022 at 18% of the overall sample. Including cross-border transactions within regions shows a much more active cross-border marketplace, totaling 142 transactions (40% of all Packaging Transactions in 2023).

Europe/Middle East/Africa (EMEA) targets saw the highest number of cross-border deals, split 60% within EMEA and 40% from outside the region. The most active non-EMEA acquirers were from Japan; within EMEA, Germany, France and Austria combined for 50% of cross-border deals.

51% of acquirers of Rest of World (ROW) targets were beyond national borders. Cross-regional deals were more common in ROW, with European buyers the most active.

On a proportional basis, North America targets saw the least amount of cross-border activity, with only 16% of acquirers outside of national borders. Non-North American acquirers were predominantly European.

As noted in our Winter Industry Insights, we see no premium or discount for cross-regional or cross- border transactions. Deal values are driven more by product segment, buyer type, deal motivation, and the pricing prevalent in target markets (regardless of buyer geography).

As the strategic value of a cross-border transaction is often significant to an acquirer, this raises the question of why no premium is ascribed to these transactions. We suggest that while the strategic value may warrant a premium, the additional risks in consummating such a transaction neutralizes that premium. Mazzone’s experience in cross-border transactions has revealed differences that must be carefully managed in these situations – not simply language and time zones, but differences in negotiation styles; legal, tax, and accounting standards; due diligence processes; regulatory approvals; and transaction timelines. All this needs to be carefully navigated to successfully close a cross-border deal.

Mazzone’s Cross Border Experience

In 2022 – 2023, approximately 30% of our transactions were cross-border, including select transactions featured below, with Mazzone advising clients from the US, Europe, the Middle East, and Asia, in the closing of transactions in the US, Mexico, and Europe.

[1] Our three tracked regions include (North America (NA), Europe/Middle East/Africa (EMEA), and Rest of World (ROW)

Industry Insights: Global Packaging Industry, Winter 2024

Relieved that much of the world’s economy avoided recession in 2023, many in the packaging industry are nonetheless happy to have 2023 in the rearview mirror. While not necessarily a retraction, many in our industry dealt with uninspiring volume, increasing costs of labor, and increasing costs of financing. This lackluster economic backdrop and recession uncertainty, coupled with significantly increased interest rates, hit the M&A transaction market hard.

Relieved that much of the world’s economy avoided recession in 2023, many in the packaging industry are nonetheless happy to have 2023 in the rearview mirror. While not necessarily a retraction, many in our industry dealt with uninspiring volume, increasing costs of labor, and increasing costs of financing. This lackluster economic backdrop and recession uncertainty, coupled with significantly increased interest rates, hit the M&A transaction market hard.

Our key observations for this edition of Industry Insights:

Transaction Volumes continued their decline from 2021, with major segments witnessing double-digit declines. Month-to-month data provide no firm indication that volumes are yet to rebound. There were, however, pockets of positive momentum in Machinery & Equipment, Multi-material Converters, and Rigid (non-plastic) packaging.

Activity dropped across all Buyer Types (corporate, private, sponsor). The one ray of hope was an actual uptick in new sponsor-led platform formation – with new platforms slightly surpassing pre-pandemic levels.

Average deal pricing (as measured by EBITDA multiples) slid for the second year in a row, falling by more than one turn of EBITDA to 8.0x. All segments are trading at or below their five-year average pricing. This may signal an opportunity for motivated acquirers to move back into the market (see above – new platforms).

It is now clear that the aberration was not suppressed numbers in 2023, but rather over exuberance in prior years (primarily 2021). 2023’s volumes and pricing more closely resemble the Covid year of 2020. With the market anticipating central banks to cut interest rates in 2024, there’s optimism that the opportunities for acquisitions can improve, and a solidifying of demand/pricing could also translate to normalization of the M&A environment. When we will see the results of this, however, is not yet clear.

There were a number of transactions that were brought to market in 2023 but did not meet the expectations of the Sellers and remain on hold. It remains to be seen what will happen first: (i) Sellers adjust their expectations so that these deals can close, or (ii) if falling interest rates and an improved economic environment return multiples to 9.0x+. If we must wait for an improved environment, deal volumes are not likely to rebound meaningfully until 2025.

While short of 2021’s blow-out year for new Sponsor Platforms, 2023 saw a 15% increase in new platform formation by financial sponsors, bringing new platform formation in line+ to activity in 2019 - 2020. Perhaps sensing a “buy low” opportunity, sponsors executed buyouts at a 2.1x discount to multiples that they paid in 2022. While still early in the cycle, this is an indication that we may have reached a “bottom” and activity may be poised to bounce back.

Recent Packaging Industry Transactions

Unlocking Success: Navigating the Waves of Private Equity Trends and Beyond

Coming out of an annual review of private equity buyouts and recapitalizations, we delve into the major trends impacting deal volumes, valuations, due diligence, and the credit environment in private equity throughout 2023. Understanding these trends is crucial for anticipating the trajectory of private equity deal activity as we venture into 2024.

Coming out of an annual review of private equity buyouts and recapitalizations, we delve into the major trends impacting deal volumes, valuations, due diligence, and the credit environment in private equity throughout 2023. Understanding these trends is crucial for anticipating the trajectory of private equity deal activity as we venture into 2024.

Deal Volumes: Balancing Quality and Quantity

In 2023, private equity deal volumes have been marked by a delicate balance between quality and quantity. While the market has seen robust activity, investors are placing a heightened emphasis on securing deals that align with strategic objectives. Quality targets that offer resilience and growth potential are in focus, leading to a nuanced approach to deal selection.

Global Private Equity Transaction Activity (Source: Pitchbook)

Although many pundits suggest private equity activity has fallen off the cliff, deal volumes in 2023 still exceeded pre-2021 levels. With optimism in a soft-landing here in the U.S. and improving credit markets, market participants are optimistic that 2023 levels will be met, if not exceeded.

The total value of transactions saw a further drop as the the debt capital markets impacted private and institutionally backed owners of larger companies more heavily versus those in the lower middle market. Many of these owners have stayed on the sidelines for the exit.

Softness in commercial activity for some owners/operators (see: destocking, consumer discretionary markets, building products/services, et. al.) paused many owners/operators to come to market in 2023; however, anticipation of more normal periods ahead in 2024 and 2025 has created optimism for transactions going forward.

Private Equity Activity Heavy in South/Southeast

As we enter the 2024 conference season, we will be exhibiting and attending ACG's M&A South with over 200 private equity groups looking for more deal flow and transacting here in the South/Southeast U.S. This region has continued to be the most active region sought after by private equity, representing over 31% or nearly 1/3 of all PE transactions in 2023. This is relatively unsurprising as this region has the led the charge for PE activity over the last few years.

PE Transactions by Region - U.S. (Pitchbook)

Valuations: Keeping Perspective

Valuations have been a focal point in 2023, with a dichotomy between buyers and sellers. As cost of capital has increased across the world, private equity and buyers across the landscape have adjusted valuations downwards to meet equity returns and sellers have been reticent to move off record valuations seen in 2021. For owners out there looking to transact, striking the right balance between growth potential and realistic valuations is paramount.

Median North America and Europe PE buyout EV/EBITDA multiples (Pitchbook)

Key Takeaways:

Keeping Perspective: Median valuations dropped ~1.6x EV/EBITDA in North America and Europe, comparing 2022 to 2023. 2023 valuations ended up slightly below the 10 year avg. of 11.1x EV/EBITDA. This past year saw the PE buyout world revert to the norm versus what many of the pundits may suggest.

Valuation Trends by Region: European buyout valuations felt the global credit and macro impacts more than North American buyouts where valuations dropped to lowest levels since 2016. Although North America buyouts dropped from record levels of 2022 and 2021, valuation levels still exceeded every other period (2013-2020) over the last ten years.

Credit Market Moves

The most impacted segment of transactions were larger LBOs which saw average leverage decrease by ~1.5x. During the overheating of the debt capital markets post-COVID, 6.0x+ Debt/EBITDA or leverage for $20mm EBITDA businesses and above was expected; however, leverage on debt transactions averaged ~4.5x. Also, lenders were more cautious in underwriting LBOs throughout 2023 with increased fixed charge ratios and an uncertain macro environment. Debt/EV ratios fell over 500 basis points to 45.7%, the lowest debt/EV ratio over the last 10 years.

Debt Percent (LCD) of NA and Europe PE buyouts

Private Equity Carveouts are Building Momentum

Since Q4 2021, many have been predicting carveouts to increase; however, momentum has started to ramp up more quickly here in the last two quarters of 2023. Since 2018, only two quarters saw higher percentages of PE carveout activity than Q4 2023.

Similarly, we are seeing private equity groups reach out more frequently to explore carveouts of non-core operations within their core platforms, many of whom have been very active on acquisitions over the last 10 years. Anecdotally, we are seeing this more frequently discussed as part of plans for a greater exit down the line or recapitalization anticipated here in 2024. We have worked on over 4 carveouts since later in 2022 and anticipate this activity to continue.

PE Carveouts as a % of Buyouts (Pitchbook)

Due Diligence Trends: Tech-Enabled and Return to Comprehensive Diligence

Due diligence processes are undergoing a tech-enabled transformation. Dataroom and other due diligence workstreams continue to explore more streamlined approaches to the deal process. ESG diligence has gained momentum, especially from global private equity groups and those overseas buyers with more regulatory and oversight reporting required. There was a period in 2021 and early 2022 where diligence red flags were quickly dissolved; however, these issues are impacting deals and valuation more heavily today versus the recent past.

Anticipated Impact on 2024:

Looking ahead to 2024, everyone is watching the credit markets and the lending environment to see how aggressively these moves will impact leverage, cost of capital and valuations. We are seeing many smart owners and operators work with their advisors early to work on what they can control and put their business in the best position to seek a liquidity or growth equity transaction. We expect these trends to continue.

Mazzone advises Chicago Industrial Fasteners on its sale to AFC Industries, a portfolio company of Bertram Capital Management

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to Chicago Industrial Fasteners, LLC (“CIF”) with respect to its sale to AFC Industries (“AFC”), a portfolio company of Bertram Capital Management. This is the fifth industrial transaction completed by Mazzone in 2023.

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to Chicago Industrial Fasteners, LLC (“CIF”) with respect to its sale to AFC Industries (“AFC”), a portfolio company of Bertram Capital Management. This is the fifth industrial transaction completed by Mazzone in 2023.

CIF is a leading distributor of specialty and standard fasteners throughout North America. Based out of West Chicago, IL, CIF serves OEMs, hardware providers, and material fabricators across a diverse range of industries including heavy truck, wind and solar generation, defense, and automotive. Products supplied span from multi-processed blueprint custom parts to high-volume common fasteners.

“This new chapter with AFC opens the door for us to continue to expand the solutions we can provide for our customers. It is exciting to have more resources to keep building on the foundation of service, teamwork, and partnership that we have established over the past 20 years,” noted John Price, cofounder of CIF. “The Mazzone team was integral at all stages of the sale process and helped us close quickly and efficiently.”

Cathy Price, co-founder of CIF commented, “Mazzone began advising us more than a year before we started the sale process. Their advice helped strengthen our business, which allowed us to be better prepared for the sale process and achieve an extraordinary outcome.”

“In CIF we found a business built around the same core commitment to providing excellent service that we strive for at AFC," said AFC CEO Kevin Godin. "The more we got to know John and Cathy and their team the more obvious it was that this was a great fit. Both of these businesses are better together, each brings key resources and capabilities that strengthen the other.”

Dustin Ramsey, Director at Mazzone, noted, “It was an honor working with John and Cathy on the transaction. They were passionate about finding the right home for their business and team, and we believe AFC is the right partner for them.”

About CIF

Chicago Industrial Fasteners was founded in 2003 and specializes in supplying difficult to produce, and often low-volume, products that many other competitors are unable or unwilling to provide. CIF’s robust vendor network and on-hand inventory selection allows them provide mission critical parts to customers on short notice, keeping their operations moving. For more information, please visit cifbolts.com.

About AFC

Headquartered in West Chester, OH, AFC Industries is a dynamic organization dedicated to providing supply chain management solutions on small components and tooling for a diverse base of manufacturers and assemblers across a broad range of industries. Through its experienced team and global resources, AFC excels at making customer manufacturing and assembly processes more efficient and cost-effective. For more information, please visit afcind.com.

Connect with one of our advisors

Enter your email below to connect with a member of our industrials team.

Mazzone advises Pamarco on the divestiture of its Palmyra operations to Precision Roll Solutions, a portfolio company of Guardian Capital Partners

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to Pamarco Global Graphics, Inc. (“Pamarco” or the “Company”), a leading provider of proven technology solutions for the global packaging, industrial coatings, commercial printing, and original equipment manufacturing industries, on Pamarco’s divestiture of certain mechanical engraving and gravure print assets previously located in Palmyra, NJ to Precision Roll Solutions (“PRS”), a portfolio company of Guardian Capital Partners.

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to Pamarco Global Graphics, Inc. (“Pamarco” or the “Company”), a leading provider of proven technology solutions for the global packaging, industrial coatings, commercial printing, and original equipment manufacturing industries, on Pamarco’s divestiture of certain mechanical engraving and gravure print assets previously located in Palmyra, NJ to Precision Roll Solutions (“PRS”), a portfolio company of Guardian Capital Partners.

Pamarco’s presence in Palmyra was established through its acquisition of Armotek Industries, Inc. in 1996. Since, Pamarco Palmyra has established a strong reputation as a producer of rolls used by customers in the engraving, gravure, and embossing industries, demonstrated by the Company’s long-tenured blue-chip customer relationships spanning a wide array of pharmaceutical, consumer staples, and other industrial end-market applications.

Allan Li, CEO of Pamarco, noted, “Firstly, Pamarco is proud of the operations and the brand that our employees have built in Palmyra over the past 25 plus years. Ultimately, the divestiture of the niche assets held in Palmyra will allow Pamarco to focus on its core competencies in the laser engraved anilox and engineered technology categories, which aligns with Pamarco’s long-term growth strategy. The Mazzone team proved again to be essential in working through the intricacies of a transaction that involved a complex transition period and a variety of unique nuances.”

John Burgess, Pamarco’s President, commented, “The sale of these assets to PRS is a strategic move made in conjunction with the recent acquisition of TLS in Germany to allow Pamarco to focus and strengthen its worldwide anilox business. We appreciate the Mazzone team’s dedication to executing both of these transactions in an efficient and effective manner.”

Dustin Dawson, Vice President at Mazzone, added, “We are pleased to announce another strategic transaction with the Pamarco team, particularly as this deal falls right on the heels of the October acquisition of TLS. Pamarco is rapidly positioning itself as the global leader in the laser engraved anilox technologies category, and this divestiture is one more step towards that ultimate goal.”

Managing Director Maury Bell and Vice President Dustin Dawson were lead team members on the transaction.

About Pamarco

Founded in 1946, Pamarco is a leading provider of proven technology solutions for the global printing, packaging, and converting industries. Pamarco designs, manufactures, and distributes a broad portfolio of aftermarket products that includes anilox and gravure rollers, carbon fiber chambered doctor blades, and precision equipment and accessories for print systems. Pamarco services a variety of growing markets, including global packaging, industrial coatings, commercial printing and OEMs in North America, Europe, and other global regions using its leading brand names and multiple channels to market. Pamarco’s established premium brands, including E-Flo and ThermaFlo anilox rolls, Absolute doctor blades, and Sentinel ink management systems, represent the industry standard in quality, efficiency, and precision. For more information, please visit www.pamarco.com.

About PRS

PRS is a full-service provider of highly-engineered precision roll solutions and related process componentry utilized within a variety of manufacturing environments. The Company’s components are used to coat, cut, convey, press, heat, cool, emboss, and engrave various substrates which supports the production of thousands of end-use products spanning a wide array of consumer products, life sciences, and other industrial end-market applications. For more information, please visit www.precisionrollsolutions.com.

About Guardian Capital Partners

Guardian Capital Partners is an operationally focused private equity firm based in suburban Philadelphia. Guardian makes control investments in lower middle market consumer, niche manufacturing, and specialty business services companies. Guardian partners with management teams to provide equity capital to fuel the growth of privately held businesses. Guardian believes the private equity experience and complementary skill sets of the Guardian team provide a unique combination of operating and finance capabilities resulting in certainty of execution and meaningful long-term value creation for its portfolio companies. For more information, please visit www.guardiancp.com.

Mazzone advises Pamarco on its acquisition of TLS

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to Pamarco Global Graphics, Inc. (“Pamarco” or the “Company”), a leading provider of proven technology solutions for the global packaging, industrial coatings, commercial printing, and original equipment manufacturing industries, on the further expansion of its European presence through the acquisition of TLS Anilox GmbH and TLS Invest GmbH (together “TLS”), a leading provider of anilox rolls and related equipment headquartered in Salzkotten, Germany.

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to Pamarco Global Graphics, Inc. (“Pamarco” or the “Company”), a leading provider of proven technology solutions for the global packaging, industrial coatings, commercial printing, and original equipment manufacturing industries, on the further expansion of its European presence through the acquisition of TLS Anilox GmbH and TLS Invest GmbH (together “TLS”), a leading provider of anilox rolls and related equipment headquartered in Salzkotten, Germany.

John Burgess, Pamarco’s President, noted, “For Pamarco this acquisition represents a key strategic objective of ours to have a full service anilox producer in the heart of the European market to better service the converting and OEM customer base. TLS has an excellent quality and service reputation and a world-class sales & distribution network, which we will combine with our own to give us unsurpassed coverage in Europe and beyond. The Mazzone teams’ counsel and analysis during this acquisition process was invaluable.”

Allan Li, CEO of Pamarco and Director at Kotts Capital Holdings, the family office holding company that owns Pamarco, added, “We are extremely excited to welcome TLS, its employees, and its customers to the Pamarco family, and we look forward to strengthening our position as the trusted supplier to our customers by providing value added products and services to both new and existing customers globally. We’ve worked with Mazzone and its team members for over 20 years on numerous deals, and the team’s guidance proved again to be instrumental, particularly given the complexities involved with an international acquisition in Germany.”

Dustin Dawson, Vice President at Mazzone, commented, “It was a pleasure working with the Pamarco team to bring this one to a happy outcome. The TLS deal exemplifies Pamarco’s acquisition strategy of growing the Company’s global footprint and diversifying its end market exposure, while adding to its portfolio of leading technologies.”

Managing Director Maury Bell and Vice President Dustin Dawson were lead team members on the transaction.

The transaction marks Mazzone’s eighth cross-border deal since 2019.

About Pamarco

Founded in 1946, Pamarco is a leading provider of proven technology solutions for the global printing, packaging, and converting industries. Pamarco designs, manufactures, and distributes a broad portfolio of aftermarket products that includes anilox and gravure rollers, carbon fiber chambered doctor blades, and precision equipment and accessories for print systems. Pamarco services a variety of growing markets, including global packaging, industrial coatings, commercial printing and OEMs in North America, Europe, and other global regions using its leading brand names and multiple channels to market. Pamarco’s established premium brands, including E-Flo and ThermaFlo anilox rolls, Absolute doctor blades, and Sentinel ink management systems, represent the industry standard in quality, efficiency, and precision. For more information, please visit www.pamarco.com.

About TLS

Since 2009, TLS has provided high-quality, innovative anilox rolls and anilox roll sleeves with solutions in the printing and coating industry that are customized for the customer. TLS experts have developed an extensive range of individual laser engravings that are designed to meet even the most demanding requirements of modern flexographic printing: high-quality solid surfaces, fine lettering, reverse texts, opaque white, multi-color printing with low color gamut, etc. TLS aims to continuously push the limits in engraving technology. For more information, please visit www.tlsanilox.com.

Key Takeaways from Pack Expo 2023

Managing Director Jonathan White shares his key takeaways from Pack Expo Las Vegas, where the mood was slightly subdued due to flattish volumes reported by companies across the Packaging Industry. Lower volume was somewhat mitigated by improved margins resulting from decreases in cost inputs, which have yet to be passed along to customers. However, customers will eventually be clawing back these cost decreases, and Mazzone is keeping a close eye on the timing of these claw backs versus the rebound in volumes to determine the best time for our clients to enter the marketplace.

Managing Director Jonathan White shares his key takeaways from Pack Expo Las Vegas, where the mood was slightly subdued due to flattish volumes reported by companies across the Packaging Industry. Lower volume was somewhat mitigated by improved margins resulting from decreases in cost inputs, which have yet to be passed along to customers. However, customers will eventually be clawing back these cost decreases, and Mazzone is keeping a close eye on the timing of these claw backs versus the rebound in volumes to determine the best time for our clients to enter the marketplace.

In our latest edition of Industry Insights: Global Packaging, we noted that Packaging Industry transaction volume and pricing have been down, and this was reflected anecdotally by companies we spoke with at Pack Expo that have transactions lingering in the marketplace due to the bid-ask gap between buyers and the sellers. Mazzone believes buyers are being conservative on valuations due to aforementioned low volumes and a concern over margins—with cost input decreases impacting margins in the present, is the data sufficiently transparent for the buyer to understand the sustainable margin of the business going forward? We saw indications of rebounding activity late this summer but don’t anticipate a sustained shift until Q1 of 2024 when mounting pressures to complete transactions force dealmakers to find a way to get the deal done.

Industry Insights: Global Packaging Industry, Summer 2023

As the Industry heads to Pack Expo in September, Mazzone & Associates provides our semi-annual update on Mergers & Acquisitions activity in the Packaging Industry.

As the Industry heads to Pack Expo in September, Mazzone & Associates provides our semi-annual update on Mergers & Acquisitions activity in the Packaging Industry. Key observations for this edition of Industry Insights:

Transaction Volumes are down from 2022: -7% for the trailing four quarters (June 2023) and -13% for the annualized run rate. There are signs, however, that volumes will bounce back in the second half of this year (p. 2).

EBITDA Multiples are down year-over-year, normalizing to the mean of the last five years. While EBITDA Multiples are down, Revenue Multiples are up, signaling shifts in profitability of transacted companies (p. 4).

Financial Sponsors, both as strategic add-on acquirers and new platform buyers, remain very active, whereas Private and Corporate Buyers are being less aggressive (p. 5).

Overall Cross-Regional M&A is consistent with prior years, but shifts in Target Geographies favor EMEA and ROW (Rest of World) versus North America (p. 6).

Public Company valuations have not shifted significantly over the last year and remain at the lower end of their trading range for the past decade (pp. 6-7).

Recent Packaging Industry Transactions

Mazzone advises FINE Parking Group and ValorBridge Partners on FINE’s acquisition of Preflight Hobby

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to FINE Parking Group (“FINE”) and ValorBridge Partners (“ValorBridge”) with respect to FINE’s acquisition of PreFlight Airport Parking’s facility at William P. Hobby Airport in Houston, Texas (“PreFlight Hobby”).

PreFlight Hobby is a 1,400-space multi-story parking garage that is conveniently located next door to FINE’s existing facility at the Houston Hobby airport; the combination of the facilities would establish FINE as the premier off-airport parking operator at Hobby and increase brand presence in the greater Houston market.

“We are excited to announce the addition of another location to our growing portfolio of off-airport parking facilities,” said Chris Amburgy, CEO of FINE. “PreFlight Hobby’s location, being adjacent to FINE’s existing facility at Hobby airport, is a particularly strong strategic fit. Opportunities for shared services, expanded capacity, and operational efficiencies across the facilities provide unique upside, and will ultimately allow the FINE brand to further improve the parking experience for travelers in the Houston area.”

July 2023 Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as the exclusive financial advisor to FINE Parking Group (“FINE”) and ValorBridge Partners (“ValorBridge”) with respect to FINE’s acquisition of PreFlight Airport Parking’s facility at William P. Hobby Airport in Houston, Texas (“PreFlight Hobby”).

PreFlight Hobby is a 1,400-space multi-story parking garage that is conveniently located next door to FINE’s existing facility at the Houston Hobby airport; the combination of the facilities would establish FINE as the premier off-airport parking operator at Hobby and increase brand presence in the greater Houston market.

“We are excited to announce the addition of another location to our growing portfolio of off-airport parking facilities,” said Chris Amburgy, CEO of FINE. “PreFlight Hobby’s location, being adjacent to FINE’s existing facility at Hobby airport, is a particularly strong strategic fit. Opportunities for shared services, expanded capacity, and operational efficiencies across the facilities provide unique upside, and will ultimately allow the FINE brand to further improve the parking experience for travelers in the Houston area.”

Chris Durham, General Manager of ValorBridge, added, “The acquisition of PreFlight Hobby falls solidly within our thesis for FINE’s expansion; a greater presence in the Houston market will drive customer loyalty as more travelers are able to experience FINE’s stress-free, high-end parking experience. Mazzone has long provided corporate development advisory services across our portfolio, and the attentive service provided throughout this latest acquisition only reiterates the Mazzone team’s expertise in seamlessly executing transactions.”

Kansas City-based UMB Financial Corporation provided senior debt financing on the acquisition. Terms of the transaction were not disclosed.

Dom Mazzone, Managing Director; Dustin Dawson, Vice President; and Ryan Durham, Associate were lead team members on the transaction.

About FINE

FINE Parking Group is the owner and operator of five premium off-airport parking facilities located at Denver International Airport, Tulsa International Airport, and William P. Hobby and George Bush Intercontinental Airports in Houston. FINE’s emphasized focus on the customer experience yields the trust and consistency that has facilitated the growth of a loyal customer base across the Company’s geographies. On-site auto detailing, valet parking, an easy-to-use customer app, and loyalty programs are just a few of the additional resources that the FINE brand is known for.

FINE continues to actively seek opportunities for the acquisition or development of airport and urban parking facilities in markets with favorable and sustainable growth characteristics. Please contact Dustin Dawson at ddawson@mazzoneib.com with any prospective opportunities.

About ValorBridge Partners

ValorBridge Partners is an Atlanta-based private evergreen holding company that owns, operates, and invests in healthcare, financial services, real estate, and industrial supplies and service companies. With a track record spanning over two decades, ValorBridge’s uncommon combination of substantial entrepreneurial, operational, and classic value investing experiences, as well as its long-term orientation as an investor, have positioned the company as a strong partner in providing capital to growing companies. ValorBridge also offers a wealth of strategic guidance and experience gained from successfully growing companies at all stages of the business life cycle.

Mazzone Industry Insights: Environmental Services — A Deep Dive into Waste, Recycling, and Sustainable Solutions

In this edition of our Industry insights, we will be focusing on recent developments and trends in the environmental services sector in the middle market. The environmental services industry—which includes companies that provide services such as waste management, environmental ancillary services and related products (inspection, preservation, remediation and testing), recycling, and closed loop models—has seen steady growth in recent years, driven by increased regulatory requirements and a growing attention towards environmental preservation and of the importance of sustainability, which, in turn, have created larger markets for sustainability-focused models.

In this edition of our Industry insights, we will be focusing on recent developments and trends in the environmental services sector in the middle market. The environmental services industry—which includes companies that provide services such as waste management, environmental ancillary services and related products (inspection, preservation, remediation and testing), recycling, and closed loop models—has seen steady growth in recent years, driven by increased regulatory requirements and a growing attention towards environmental preservation and of the importance of sustainability, which, in turn, have created larger markets for sustainability-focused models.

Mazzone advises TSC Auto ID Technology with respect to the acquisition of a producer of labels and shrink sleeves located in Poland

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to TSC Auto ID Technology Company (“TSC”) with respect to its acquisition of a producer of labels and shrink sleeves located in Poland (“the Company”).

The Company is a privately held producer of TTR Tapes, unprinted labels, flexographic printed labels, and shrink sleeves for the Polish and European market. The Company also offers label printers, code scanners, mobile terminals, and RFID technology for its customers. Operations are conducted in two facilities strategically located in Poland.

June 2023 Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to TSC Auto ID Technology Company (“TSC”) with respect to its acquisition of a producer of labels and shrink sleeves located in Poland (“the Company”).

The Company is a privately held producer of TTR Tapes, unprinted labels, flexographic printed labels, and shrink sleeves for the Polish and European market. The Company also offers label printers, code scanners, mobile terminals, and RFID technology for its customers. Operations are conducted in two facilities strategically located in Poland.

John Otott, Global General Manager of Consumables for TSC, noted that “the combination of our two organizations will allow TSC to better serve our European customer base with genuine OEM supplies in addition to our extensive portfolio of hardware to deliver complete, reliable, and high-quality label printing. We selected Mazzone to assist us in this transaction, as their understanding of both the market and how to get deals done in a challenging environment was key to our success. Furthermore, their ability to break down complex deal dynamics into simple solutions allowed us to reach a successful transaction.”

Jonathan White, Managing Director at Mazzone, noted, “We are pleased to have the opportunity to partner with TSC and guide them through this cross-border acquisition. This combination will undoubtedly move TSC’s strategy forward and also create opportunities for the Company. TSC will be a great partner for the Company and its employees, and we are eager to see what they will accomplish together.”

Jonathan White, Managing Director; Stuart Sanford, Director; and Ryan Durham, Associate were lead team members on this transaction.

About TSC

Serving customers in over 100 countries, TSC Auto ID Technology Company (Taiwan Stock Exchange: 3611) is a leading designer and manufacturer of innovative asset tracking and identification solutions, including mobile, desktop, industrial and enterprise-grade barcode label printers, RFID printers, barcode label inspection systems, print engines, and genuine supplies. With one of the industry’s most comprehensive selection of barcode label printers, TSC provides solutions for transportation and logistics, retail, manufacturing, food and beverage, healthcare, and automotive companies seeking world-class, innovative, and high-performance tracking and identification solutions. With over 6 million printers sold around the world, TSC is committed to providing strong local sales engineering support, continuous investment in new product development, and quick solutions to meet the needs of small and medium-sized businesses and Fortune 500 companies around the world. For more information, please visit www.tscprinters.com.

Mazzone Industry Insights: Labels

Acquisitions in the Label Market have been on a tear for the last five to ten years, with Mazzone’s tracked transaction volumes increasing from 30 in each of 2018 and 2019 to a peak of 70 transactions in 2021. 2022 activity retreated -7%, roughly in line with Packaging Overall (-9%) and relatively resilient as compared to transactions across the broader economy (-20%).

Acquisitions in the Label Market have been on a tear for the last five to ten years, with Mazzone’s tracked transaction volumes increasing from 30 in each of 2018 and 2019 to a peak of 70 transactions in 2021. 2022 activity retreated -7%, roughly in line with Packaging Overall (-9%) and relatively resilient as compared to transactions across the broader economy (-20%).

The cooling off reflects increases in inflation and interest rates as well as fears of recession (please refer to Mazzone’s Winter 2023 Global Packaging Insights). This is particularly evident in the quarterly data: in the six quarters beginning Q1-21, the average transaction count was 18.5; each of the last three quarters ending March 2023 had “only” 12 transactions (-35%).

Mazzone advises Precision Machining Group, a Trivest Partners portfolio company, on its sale to The Boler Company

Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to Precision Machining Group Corporation (“PMG” or the “Company”), a portfolio company of Trivest Partners (“Trivest”), with respect to the sale of PMG to The Boler Company (“Boler”).

PMG is a leading manufacturer of diversified CNC precision machined components for blue-chip customers across the U.S. With over 200 employees, the Company manufactures mission-critical components for OEM’s and Tier 1 suppliers in the fluid power, material handling, agriculture, industrial, oil & gas, and aerospace verticals.

April 2023 Mazzone & Associates (“Mazzone”) is pleased to announce that it acted as exclusive financial advisor to Precision Machining Group Corporation (“PMG” or the “Company”), a portfolio company of Trivest Partners (“Trivest”), with respect to the sale of PMG to The Boler Company (“Boler”).

PMG is a leading manufacturer of diversified CNC precision machined components for blue-chip customers across the U.S. With over 200 employees, the Company manufactures mission-critical components for OEM’s and Tier 1 suppliers in the fluid power, material handling, agriculture, industrial, oil & gas, and aerospace verticals.

“Boler represents an ideal partner for PMG’s future,” said Alex Vogl, CEO of PMG. “Boler brings industry expertise and a long-term investment strategy to bear that will aid PMG in continuing its growth trajectory, while remaining committed to ‘Get Every Part Right.’ The Mazzone team was a pleasure to work with and expertly guided us throughout the entire process, achieving a great outcome for everyone involved.”

Trivest acquired PMG in 2014, and during the investment period, PMG completed multiple add-on acquisitions and drove significant organic growth. Todd Jerles, Partner at Trivest, reflected, “Mazzone served as a trusted advisor throughout the transaction preparation and sales process. Their advice, hard work, and dedication proved highly valuable in achieving a successful outcome.”

Dustin Ramsey, Director at Mazzone, noted, “It was a pleasure working with the PMG and Trivest teams on this transaction. Together, they built a truly differentiated company, and PMG is poised for continued success with Boler.”

About Precision Machining Group

Precision Machining Group was created in 2014 with the goal of acquiring CNC precision machining businesses considered market leaders in their respective industries. PMG leverages its three U.S.-based, ISO-certified manufacturing plants, as well as a global network of manufacturing partners, to offer its customers domestic, nearshore, and offshore solutions. Its long-term customer base consists of a diversified group of Tier 1 suppliers and OEMs that rely on PMG to supply mission critical components. PMG’s components are utilized in numerous end market applications, including fluid power, agriculture, material handling, mobility, general industrial, oil & gas, construction, and aerospace. For more information, please visit www.pmgcorp.com.

About Trivest Partners

Founded in 1981, Trivest Partners is the oldest private equity firm in the Southeast U.S. and focuses exclusively on founder and family-owned businesses. Trivest is headquartered in Miami, Florida with regional offices in Charlotte, Chicago, Los Angeles, New York, and Toronto. For more information, please visit www.trivest.com.

About The Boler Company

The Boler Company, founded in 1976, is a family enterprise with operations across the globe in manufacturing, real estate, and other holdings. The company’s global headquarters is in Schaumburg, Illinois. The Boler Company acquired its first business, Hendrickson International, in 1978, which has since experienced substantial global growth. Today, the company has facilities all over the world and is a major supplier to every North American heavy-duty truck and trailer OEM, as well as to most manufacturers in Europe, Australia, South America, and Asia.